Blog

Blog

As retirement age approaches, the question that troubles many people the most is not how they will spend their free time, but rather: once retired, how can finances remain stable, income stay consistent, and life remain comfortable? This concern becomes even more pressing in a context where living costs rise rapidly, average life expectancy continues to increase, and traditional savings are no longer sufficient to preserve purchasing power. Entering retirement therefore requires a financial strategy that is more proactive, flexible, and forward-looking than ever before.

Today, the concept of “retirement” has changed significantly. Instead of a complete stop, many people now view retirement as the second phase of their career—a stage where they have more time to expand investments, build passive income streams, or begin activities that bring both profit and personal fulfillment. As a result, financial preparation for retirement should be viewed through the lens of “asset optimization” rather than merely “asset preservation.”

Retirement Finances

Retirement finances undergo major changes and require a new mindset

Upon entering retirement, active income from a salary is no longer available, while expenses such as healthcare, insurance, and daily living costs tend to increase over time. Many retirees choose bank savings as a safe option, but in reality, current interest rates are often lower than inflation, causing savings to lose value year by year. This reality calls for a new way of thinking about asset management and idle money after retirement.

An effective retirement financial strategy typically balances two parallel goals: preserving capital safely while enabling money to continue generating passive income. This approach helps maintain purchasing power and creates steady cash flow without adding work-related pressure. Therefore, retirement is actually the ideal time to build a stable income system rather than relying solely on savings accounts.

In the context of rapidly evolving global financial markets, many new investment channels have become more accessible to Vietnamese retirees. Thanks to technology and the rise of modern financial models, retirees now have more options to generate sustainable income, including small-scale investing, passive investment strategies, and fund-backed trading models—an increasingly popular trend worldwide.

What Should You Do in Retirement to Keep Your Money Growing?

What should retirees do to keep their money growing?

Building Smart Passive Income

Retirement is the stage where life experience, available time, and modern financial tools can be combined to create a stable monthly income stream.

Common options include:

- Renting out idle assets (houses, rooms, vehicles, etc.)

- Investing in mutual fund certificates or ETF portfolios

- Small-scale trading with AI support to reduce manual analysis

Many retirees have adopted a “passive income – self-operating assets” model, allowing financial tools to work in place of physical labor. With the increasing stability of technology, this model has become more efficient and accessible.

Combining Finance and Technology

The biggest difference between today’s retirees and those of 20 years ago lies in technology. Artificial intelligence (AI) makes investing safer, more accurate, and especially suitable for people who do not have much time to deeply research financial markets.

For example, many modern trading platforms use AI to:

- Automatically record trading journals

- Measure and manage risk

- Suggest suitable strategies

- Detect and warn against trading mistakes

- Optimize investment portfolios

For retirees, these tools increase confidence when investing while keeping risk under tight control.

For retirees, safety remains the top priority. Channels such as reputable corporate bonds, fixed-income fund certificates, or rental real estate offer stable returns with relatively low risk. These assets help form a “financial foundation” that is less affected by economic fluctuations.

However, relying solely on low-risk assets may result in returns that fail to keep up with rising living costs. Therefore, it is necessary to allocate a portion of the portfolio to higher-return investments while still maintaining controlled risk.

Financial experts currently recommend the “60 – 30 – 10” allocation model for retirees:

- 60% in safe assets

- 30% in growth assets

- 10% in high-return channels supported by technology and strict risk controls

This allocation balances stability and growth.

Thanks to technology, retirees no longer need large amounts of capital to invest. With just a few million VND per month, they can participate in optimized models such as:

-

ETF investing with automated strategies

-

Using AI-powered market analysis robots

-

Small-scale financial trading channels with AI support to reduce risk

The trend of “small investment, real returns” is spreading not only in Vietnam but across Asia, as it allows older investors to manage risk effectively, invest with minimal time commitment, and still generate steady income.

Should Retirees Try Financial Trading?

How can retirees enjoy life while earning additional income?

In the past, financial trading often made older individuals hesitant due to perceived risks and experience requirements. Today, the situation is different. Many modern models allow retirees to participate in markets without committing large capital—or even without using personal funds at all.

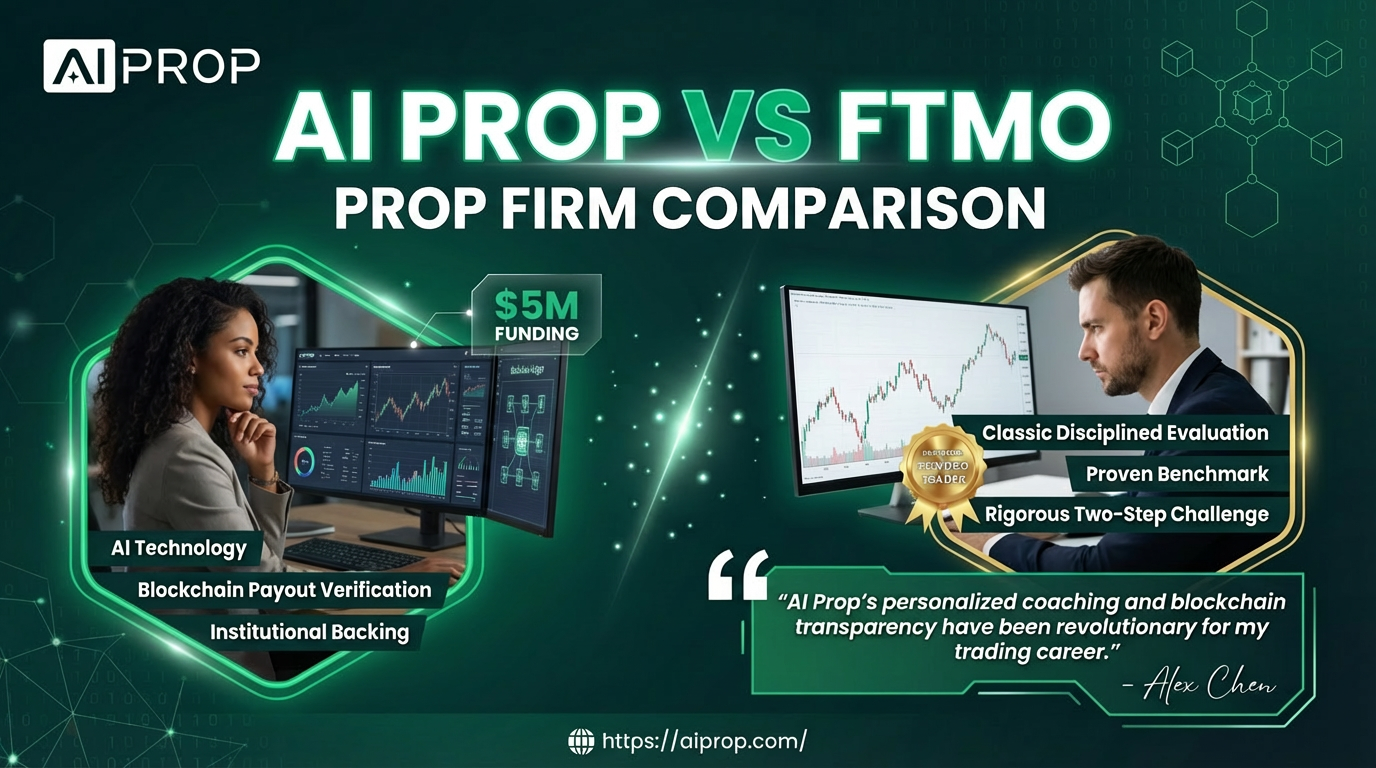

One of the most prominent global trends, especially in the US, Europe, and Asia, is prop trading: traders are provided with trading capital of up to hundreds of thousands of USD and share profits when trades are successful. With new technologies such as AI market analysis, AI-assisted decision-making, and blockchain-based transaction transparency, prop trading has become increasingly suitable for retirees seeking additional passive income while maintaining strict risk management.

Recent studies show that this model experienced explosive global growth between 2020 and 2024, with search interest increasing by over 4,000%. This clearly reflects a growing desire among people aged 50–60+ to continue earning income in a safe, smart, and systematic way.

Retirement Is a New Beginning

In reality, many people enter retirement with anxiety due to a sharp decline in income. However, when equipped with a smart financial strategy, retirement is no longer an ending—it becomes the beginning of financial freedom.

You can spend time with family, pursue hobbies, travel, and still maintain a steady income from investments—this is the ideal retirement lifestyle.

Suitable options for those seeking income after retirement include:

- Small, evenly distributed monthly investments

- AI-assisted trading to reduce analytical pressure

- Participating in prop trading models without using personal capital

- Building long-term ETF portfolios

- Or simply leveraging existing assets to generate passive income

No matter which option you choose, the most important factor is understanding your own priorities: safety, consistency, or growth. From there, select a solution that fits your risk tolerance without blindly following trends.

View retirement as an opportunity to optimize idle money, leverage new technological tools, and choose investment channels aligned with your acceptable risk level. When finances are well prepared, retirement becomes the most fulfilling stage of life—peaceful yet independent, flexible yet profitable.