Blog

Blog

Table of Content

In a discussion on Reddit, a trader described clearing $42,936 on a $200,000 funded account, passing every written rule, and requesting the payout. Then a “risk review” landed on the account. The firm later acknowledged that its first risk report had been wrong. The payout was still denied.

He didn’t blow a daily loss limit, breach drawdown, or miss a minimum trading day. He passed. The thing that took the money away wasn’t a rule he broke. It was a layer that sits on top of the rules, where a human gets to decide whether your trading “counts.” That layer has a name once you start looking for it: the discretionary review. And it’s one of the most important things to check before you ever hand a firm a challenge fee.

What actually happened

The most telling detail is the admission. According to the public thread, the firm conceded its first risk report contained an error, then declined the payout anyway. One commenter put the problem more cleanly than any terms page ever will: if the firm already admitted the first report was wrong, the real issue is no longer your hard-rule breach. It is whether a discretionary risk-review layer can override a passed account without any rule being broken.

That is the whole disease in one sentence. A review that can be invoked after you’ve passed, that doesn’t have to point at a specific broken rule, and that the firm controls end to end. When the override and the payout sit in the same hands, “you passed” stops being a guarantee and becomes an opening position.

This isn’t one unlucky account

If it were a single story, you could file it under bad luck. The same shape recurs across public trader discussion, which is why finding a top trusted prop firm is worth the effort. Read these as signals from self-reported threads, not proven facts, but the consistency is the signal.

In one thread, a trader reported having “20 accounts ready for payout” refused after the firm demanded they record themselves trading, then concluded “your strategy wasn’t a real strategy.” The same discussion carries the grim catchphrase for the whole problem: you pay a little for the ability to get denied a payout once you actually make some profit.

Elsewhere, a trader described being banned mid-trade while $19,000 in profit, with a clean record and over $110,000 already paid out across two other firms, and no specific rule breach cited. Another documented a $1,000 payout refused and two funded accounts closed over an identity-verification mix-up that was an error on the firm’s side.

None of these is “you hit your drawdown.” Each is a subjective call, made after the money was on the line, that the trader had no mechanical way to contest.

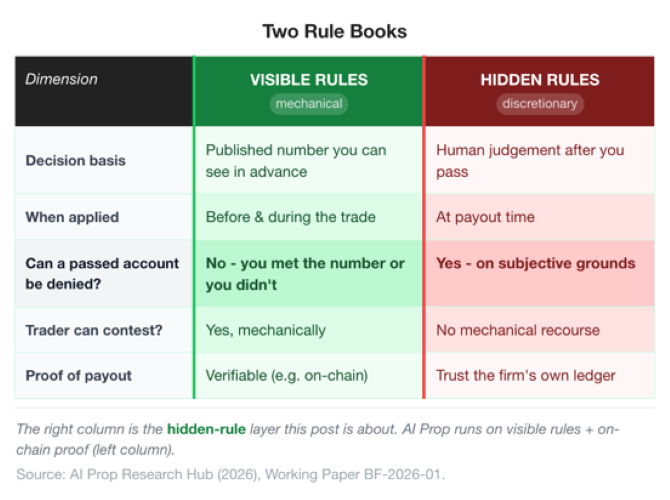

Two rule books: the one you read, and the one that denies you

Once you’ve seen enough of these stories, a pattern emerges. Most prop firms run on two separate rule books.

The first is the one on the sales page. Call these the visible rules: the daily loss limit, the maximum drawdown, the profit target, the minimum trading days. They’re mechanical and knowable in advance. You can see them before you pay, and you can trade around them. There’s nothing wrong with this book.

The second rarely makes the sales page. Call these the hidden rules: clauses buried deep in the terms, or judgement calls applied after the fact, that decide whether a passed account actually gets paid. They’re where most discretionary denials come from, because they hand the firm a reason that doesn’t map to any number you agreed to. The ones worth checking for before you buy:

- The consistency rule. Your single best day can’t exceed a set share of total profit, often somewhere in the 30-50% range. Make most of your money in one clean trade and the payout can freeze, not because you broke a risk limit, but because the firm decides your profit was too “lumpy.” One prop firm founder went on record calling it “a payout trap” rather than a genuine risk tool; in one industry survey of around 500 active traders, 53.0% named it among the features they most want to avoid.

- News-trading windows. Opening or closing inside a short window around high-impact releases, often 2-5 minutes, can void a trade. The buried part: at some firms the published terms apply this to your stop-loss or take-profit triggering inside the window too, not just manual entries.

- Minimum hold time. Close trades “too fast” and they get flagged as scalping or latency abuse and stripped out. In one documented case a firm introduced a one-minute minimum hold with no notice and applied it backwards, clawing a trader’s balance from $3,200 down to $751.

- Cross-account or group hedging. Holding opposing positions across accounts gets read as manipulation, and the winning side is denied even though no single account broke a rule.

- The catch-all. Almost every terms page carries a broad clause about “fair trading,” “good faith,” or trading that matches “real market conditions.” It names nothing specific, which is exactly the point: it’s the clause a firm reaches for when it wants to deny a payout that didn’t break any actual rule.

None of these is automatically a scam. Some are disclosed, just buried. The problem is the gap between the rule book you read before paying and the one that gets applied when you ask to be paid. And the rules can move: firms have rewritten terms mid-tenure and applied the new version to accounts that were already funded.

Why firms keep the override power

Here’s the uncomfortable economics. Every challenge fee goes into a funnel that’s brutal by design. Community discussion points to roughly 10% of traders clearing Phase 1 and only around 4% of forex traders ever reaching funded status. Treat those as a signal rather than a hard figure, but the direction is clear: the overwhelming majority of people who pay never reach a payout request at all.

Now the money on top. An industry tracker recorded about $325 million in payouts across participating firms in 2025. Even that firmer number comes with a caveat Finance Magnates states directly: the industry is unregulated and the figures are self-reported, so payout totals are “often questioned over their accuracy”. Taken at face value, it still fits the one-step model economics of the sector: revenue on volume of entries, not generosity of exits.

When most revenue arrives from people who fail, and costs spike only when someone succeeds and asks to be paid, the hidden-rule layer is the one place a firm can quietly manage that cost. Not every firm does. But the incentive to keep the option open is structural, which is why you should assume it exists until a firm proves it doesn’t.

The honest part: hard rules are fine, and good firms exist

None of this means rule enforcement is the villain. A firm that closes your account for breaching a trailing drawdown (the drawdown basics every prop trader should know) is doing its job, and you agreed to that job when you bought in. Hard rules are mechanical, knowable in advance, and you can trade around them. That’s healthy. The problem is never the rules. It’s the subjective layer that can overrule a clean pass.

And plenty of firms pay fast and clean. Some now publish fast-payout guarantees, even promising compensation if they miss the window. Others publish explicit policies stating that no rule-compliant payout will be refused. The point isn’t that the whole sector is rotten. It’s that “do they pay” is a real axis of difference, and most buyers never check it.

AI Prop has no hidden rules

The problem above was a firm being able to override an account that already passed. So a payout architecture has to remove that override surface, not bolt on more features. Everything below is one way of closing that surface. That’s the design philosophy behind AI Prop.

Start with the rules, because each interpretive rule is a place a reviewer can stand. A trailing drawdown that updates by formula leaves nothing to interpret: you either met the number or you didn’t, and the number was published before you started. No consistency rule means there’s no “your trading wasn’t a real strategy” call to make. No news-trading restriction means a normal release day can’t be reread as a violation after the fact. Take away the interpretation steps and you take away the override.

Then close the proof surface. AI Prop publishes payouts on-chain, so the record can’t be rewritten later to support a “risk review”, and anyone can verify it instead of trusting the firm’s own ledger. For the number that matters, AI Prop’s exclusive research tracked $1.7 million in verified payouts across a cohort of 978 traders in Q1 2026. That’s a measured cohort figure, not a platform-wide marketing total, and it sits on a public ledger precisely so “trust us” is never the answer. When the outcome lives outside the firm’s control, there’s nowhere for a quiet review to change it after you’ve passed.

How to protect yourself before you buy

You don’t need to read minds. You need to read terms, and ask four questions before you ever pay a fee. Can a passed account be denied at payout time, and on what specific grounds? Is there a discretionary “risk review” or “trading-style review,” and who decides it? Can you verify a payout independently, or are you trusting the firm’s own ledger? And has the firm ever changed payout terms, like a cap or a hold-time rule, after traders were already funded? A firm that answers all four cleanly has already told you most of what you need to know.

Frequently asked questions

What is a discretionary payout denial?

It’s when a prop firm refuses to pay an account that passed every written rule, on subjective grounds rather than a specific breach. Instead of “you hit your drawdown,” the reason is something interpretive: “your strategy isn’t real,” “we need you to record yourself trading,” or an internal risk review the firm controls. In the case above, a trader reported the firm even conceded its first report was wrong and still declined the payout. The defining feature is that no hard rule has to be cited, which is exactly why it’s hard to contest.

What are prop firm hidden rules?

They’re the rules that don’t make the sales page: clauses buried in the terms, or judgement calls applied after you’ve passed, that decide whether you actually get paid. The most common are the consistency rule (your best day can’t exceed a set share of total profit), news-trading windows that can void trades around high-impact releases, minimum hold times that flag fast trades as scalping, cross-account hedging bans, and a broad “fair trading” or “good faith” catch-all clause that names nothing specific. Some are disclosed but buried; the danger is the gap between the rules you read before paying and the ones applied when you ask to be paid.

Is this legal? Can they actually do that?

In most cases the discretionary language is written into the terms you agree to when you buy a challenge. The prop sector is largely unregulated, and payout figures across the industry are self-reported and “often questioned over their accuracy”. That combination, broad contractual discretion plus little outside oversight, is precisely why the burden falls on you to read the terms before buying rather than after a dispute. Some traders pursue chargebacks or public disputes, but prevention beats remedy.

How do I know if a firm has a discretionary review layer?

Read the payout section of the terms, not the marketing page. Watch for language about reviewing payouts against “prohibited trading strategies” before approval, “trading-style reviews,” or broad clauses about “manipulative” or “inconsistent” trading that aren’t tied to a numeric rule. A hard rule is mechanical and knowable in advance, reflecting how prop firms manage risk without judgement calls; a hidden rule is subjective and applied after the fact. If a firm can describe a reason to deny you that doesn’t map to a specific published number, that’s the discretionary layer. Ask directly, in writing, whether a passed account can be denied at payout and on what grounds.

Can on-chain payouts really prevent this?

They remove the place where a quiet override would hide. When a payout is recorded on a public ledger, the record can’t be rewritten after the fact to support a later “risk review,” and anyone can verify it independently rather than trusting a firm’s own numbers. AI Prop publishes payouts on-chain for exactly this reason, alongside mechanical rules with no consistency or news-trading restriction. It’s not magic. It’s just moving the proof outside the firm’s control, which is the whole point.

What questions should I ask before buying a challenge?

Four. Can a passed account be denied at payout, and on what specific grounds? Is there a discretionary “risk review,” and who decides it? Can payouts be verified independently? And can payout terms, like a cap or a hold-time rule, change after I’m funded? A firm that answers all four cleanly, in writing, has already separated itself from the pack, because most buyers never ask and most terms never volunteer the answers.

Do one thing before you trade another lot: open your prop firm’s payout terms and search for a discretionary “risk review” or “trading-style review” clause, plus any consistency, hold-time, or “fair trading” language. If you find one, you’ve found the surface that can override a clean pass. Then see AI Prop’s on-chain, verifiable payout record and mechanical rules at aiprop.com before you commit a fee anywhere.