Blog

Blog

Table of Content

You’ve had the thought. Maybe after your fourth blown account, maybe after a payout got stuck behind a clause you’d never read. The thought goes: this firm doesn’t actually want me to win. It makes its money when I fail.

You’re not paranoid. The math backs you up. Across a dataset of more than 300,000 prop trading accounts spanning ten firms, only 7.0% of traders who started an evaluation ever reached a single payout. Not 7.0% who got rich. 7.0% who saw any money at all. The other 93 in every 100 paid their fee, traded, and walked away with nothing but the receipt.

That number is the whole story, so let’s actually do the math behind it.

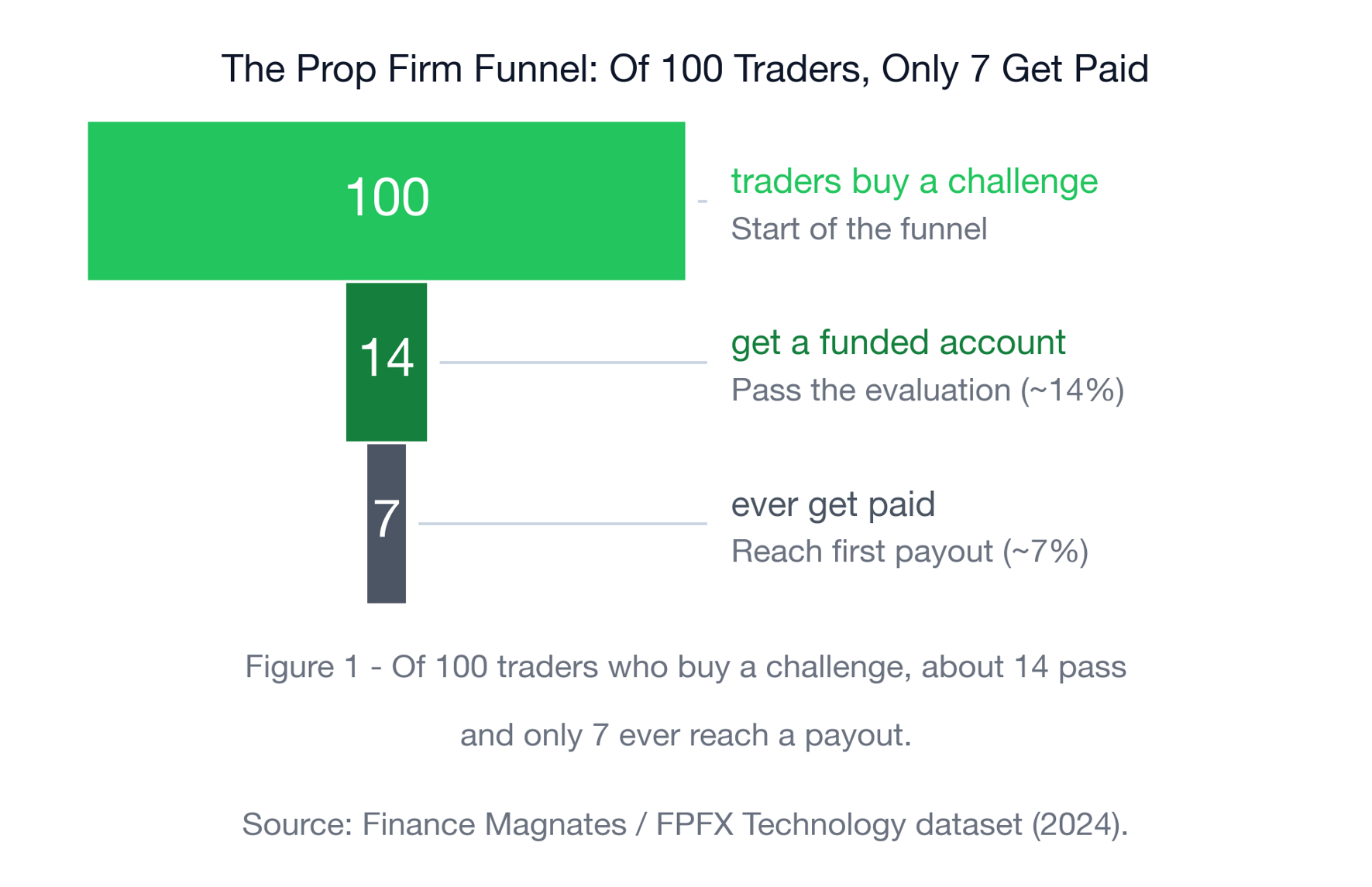

The funnel: of 100 traders who buy a challenge, 7 ever get paid

Picture 100 traders who each buy a challenge today. Here is where they end up, according to that 300,000-account dataset. About 14 of them pass the evaluation and get a funded account. Of those 14 funded traders, fewer than half, around 45.0%, ever reach a payout. Do the arithmetic and you land on roughly 7 of the original 100 who ever see a single dollar. An independent industry tracker puts the same figure at “only 7% of traders who begin an evaluation ever reach their first payout”, which is a tidy corroboration of a number most firms would rather you not picture as a funnel.

It gets sharper when you add the price tag. Because most people need more than one attempt, the realistic spend works out around $1,600 over an average of three tries at a $100,000 challenge, and across all account sizes the average outlay per account cycle lands near $800. Now stack that against the prize: when a trader does get paid, the average payout is about 4.0% of their funded account size. So a small number of people clear the bar, collect a slice, and the firm keeps a much larger pile of fees from everyone who didn’t. This is the part of the prop firm challenge guide most buyers want that almost never makes the sales page.

How do prop firms make money, fees or your profits?

Most prop firm revenue comes from challenge fees, not from a cut of trader profits, and that single fact is what tilts the incentive. Industry analysts estimate that challenge fees make up somewhere around 85.0 to 95.0% of a typical prop firm’s revenue. Treat that as an estimate, not an audited disclosure, because there is no central database of prop firm revenue and even the broad annual figures, often put at $2 to $4 billion globally, come with an explicit “no audited data exists” warning. One widely shared social-media estimate goes further, pegging last year’s challenge fees near $2.3 billion with roughly 90.0% from traders who failed, but that one is a single unverified post, so hold it loosely.

Even on the conservative read, the direction is clear. When the bulk of the money arrives the moment someone buys a challenge, a firm’s revenue stops depending on whether you eventually succeed. The structure even hedges the firm’s downside. On a $100,000 account with a 10.0% maximum drawdown, the firm’s worst-case exposure to any single trader is capped at about $10,000, while the challenge fee it collects upfront is a low-cost recurring charge against everyone who keeps failing. When the people who study this describe the model, they put it bluntly: a firm relying primarily on challenge fees rather than profits from funded traders has misaligned incentives, and the model only works correctly when funded-trader success is the primary revenue driver. That is the difference between a partner and a turnstile.

Hidden rules are how the failure gets engineered after you’ve won

The hidden rules in this industry are the instrument that lets a misaligned firm keep failing you even after you’ve passed. This series has walked through three of them. The consistency rule freezes your payout if one good day is too large a share of your total profit, which means you can hit your target and still be told no. The minimum hold time rule voids profit from trades closed too quickly, sometimes deleting your wins while keeping your losses. And the copy-trading and account flag can ban an account mid-trade on a vague technicality. Each one is a different door, but they all open onto the same room: the place where you were winning, and then a clause you never saw took it back.

The pattern isn’t a coincidence, it’s a design choice. One prop firm founder said the quiet part on the record, describing how problems arise “when rules are hidden, vague, changed retroactively, or used manually to avoid paying traders”. That isn’t an outsider’s accusation, it’s an operator describing his own industry’s playbook. And it isn’t theoretical. In one documented case, a firm introduced a minimum hold time overnight, applied it backwards to trades that were already closed, and clawed one trader’s settled balance from $3,200 down to $751.62, erasing $2,448.38 they had already earned. No bad trade caused it. A rule that didn’t exist when those trades were placed reached into the past and deleted the profit. That is what “profit from failure” looks like when it’s pointed at someone who already succeeded, and it sits in the same family as the trader denied a $42,936 payout despite breaking nothing on the page.

The honest pivot: the eval-fee model isn’t the villain

Here’s the part most takes on this topic get wrong, and the part that matters most: charging an evaluation fee is not, by itself, predatory. Every prop firm needs revenue, and a fee that filters for skill before handing over capital is a reasonable business model. AI Prop charges fees too. Pretending otherwise would be its own kind of dishonesty, and it would make everything above sound like a sales pitch instead of an argument.

It’s worth being precise about where the real damage lives, because the funnel alone doesn’t explain the anger you see in trading communities. Plenty of people fail challenges fair and square, hit a loss limit, blow an account, and own it. That stings, but it isn’t betrayal. The betrayal is the trader who’s blown a string of funded accounts and is still net negative on fees after their first real payout finally lands. It’s the person who did pass, did everything the page asked, and then watched a clause decide they didn’t. The fee isn’t what makes that story bitter. The clause is.

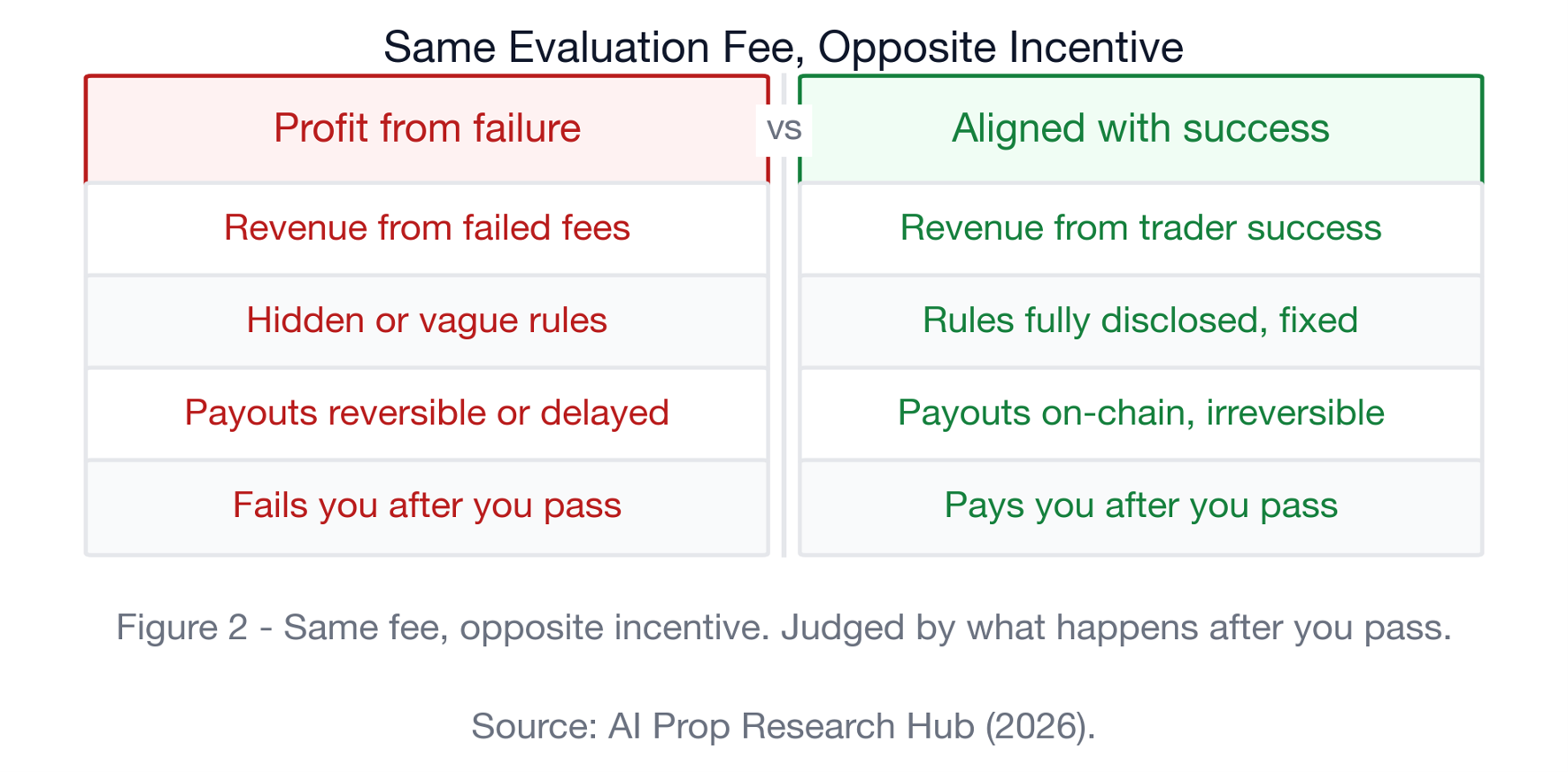

The real question isn’t whether a firm charges a fee. It’s what the firm does after you pass. A firm aligned with you makes money when you make money: it pays real payouts, scales your account, and treats your success as its revenue engine. A misaligned firm makes money when you fail, and reaches for hidden rules to keep failing you even after you’ve earned the money. Same fee at the front door, completely opposite incentive at the back. Your only job, as the person handing over the fee, is to figure out which side of that line your firm sits on before you pay, the same way you’d want to know how prop firms manage risk and what the one-step model economics actually reward before you commit.

What being aligned with you actually looks like

A firm aligned with your success removes the levers it would otherwise pull to fail you, and ties its money to a record it can’t quietly rewrite. That’s the model AI Prop is built on. It runs on Pass-First-Pay-Later, so you don’t pay the evaluation fee until you’ve actually passed, which flips the front-door risk: the firm only collects when you’ve already proven you can clear the bar. The fee still exists. You just don’t pay it into a failure.

The back door matters even more. AI Prop publishes payouts on-chain, on a public ledger anyone can verify, so a cleared payout has a transaction record and cannot be silently reversed the way a balance in a firm-controlled dashboard can. AI Prop exclusive research records $1.7 million in verified cohort payouts across n=978 traders in Q1 2026, an isolated, traceable dataset rather than a platform-wide marketing number. Worth a caveat here, because it cuts both ways: on-chain payout totals reported across the industry can include affiliates and vendors, not only traders, so a big on-chain figure is not automatically a clean trader-payout signal. What makes the AI Prop figure meaningful is that it’s tied to a specific verified cohort, not the whole wallet. And the hidden rules that did the damage above? They’re gone. AI Prop exclusive research describes a Friction Score of 0/6, meaning the six most common friction rules, the consistency rule and the minimum hold time among them, have all been removed, which is the whole point of clear-rule prop firms.

How to tell which kind you’re dealing with

You can usually spot the difference before you pay, if you check three things. First, read the withdrawal terms before you hand over a fee, not after you pass. The clause that decides whether a passed account gets paid lives in the fine print, and five minutes of reading beats a frozen payout. Second, ask whether a cleared payout is reversible. If the money sits on a ledger the firm fully controls, it can be adjusted, delayed, or clawed back. If it’s on-chain, it can’t be quietly undone. Third, check whether the rules are fully disclosed and fixed, or vague and changeable. A firm that can rewrite the rulebook mid-account, and apply the change backwards, has told you exactly what it will do under pressure. Those three checks are the practical test, and they’re worth doing every time you compare prop firms or weigh up the safest prop firm for payouts before committing a cent.

Frequently asked questions

Do prop firms want you to fail?

Many of them, structurally, benefit when you do, which is different from a person actively rooting against you. When most of a firm’s revenue comes from challenge fees rather than a cut of trader profits, its income doesn’t depend on your long-term success, and the worst-case cost of any single trader is capped while the fees keep arriving from everyone who fails. That’s a misaligned incentive baked into the model, not necessarily a conspiracy in a back room. The fix isn’t to assume malice, it’s to choose a firm whose revenue is tied to your success, where the firm only wins when you win.

How do prop firms make money?

Primarily from challenge and evaluation fees, not from sharing in trader profits. Industry analysts estimate fees make up roughly 85.0 to 95.0% of a typical prop firm’s revenue, though that’s an estimate rather than audited data, since no central database of prop firm revenue exists. The structure is profitable because most buyers never reach a payout: across a 300,000-account dataset, only about 7.0% of traders who start an evaluation ever get paid. A smaller revenue stream comes from the profit split on funded traders who do succeed, which is exactly the stream an aligned firm wants to grow.

Are prop firms a scam?

Not inherently, but the model can be run in predatory ways, and that’s the distinction that matters. Charging a fee to evaluate a trader before funding them is a legitimate business model. It tips into something worse when a firm leans on hidden, vague, or retroactively changed rules to avoid paying traders who passed, a practice one prop firm founder described on the record. In one documented case, a firm clawed a settled balance from $3,200 to $751.62 using a rule applied backwards. So the honest answer is: the model is legitimate, but firms vary enormously, and your job is to read the withdrawal terms and check whether payouts are reversible before you pay.

What percentage of traders actually get paid by a prop firm?

About 7.0%, based on the largest public dataset available. Across more than 300,000 accounts spanning ten firms, roughly 14.0% of traders passed the challenge and got funded, and fewer than half of those funded traders, around 45.0%, ever reached a payout, which nets out to about 7 in every 100 who began. An independent tracker reports the same 7.0% figure for traders reaching their first payout. It’s worth knowing that around half of funded accounts are lost within 90 days too, so getting funded is the middle of the funnel, not the end of it.

Is paying for a prop firm challenge worth it?

It can be, but only if you go in with the funnel and the fine print in view. The average trader spends around $800 per cycle and closer to $1,600 across an average of three attempts at a $100,000 challenge, and only about 7.0% ever reach a payout. That doesn’t make it a bad bet, but it makes the firm you choose the most important variable. A challenge is worth far more when the firm pays reliably, discloses its rules, and can’t reverse a cleared payout, which is why reading the withdrawal terms first is the most valuable five minutes in the whole process.

How is AI Prop different?

AI Prop is structured so the firm makes money when you do, not when you fail. It runs on Pass-First-Pay-Later, so you don’t pay the evaluation fee until you’ve passed. It publishes payouts on-chain, so a cleared payout is publicly verifiable and can’t be silently reversed. And it carries a Friction Score of 0/6, meaning the six most common friction rules, including the consistency rule and minimum hold time, have been removed. AI Prop exclusive research records $1.7 million in verified cohort payouts across n=978 traders in Q1 2026. AI Prop still charges fees, like any firm, but the incentive sits on the side of your success rather than your failure.

What’s the single biggest red flag to watch for?

Rules that can be changed after you’ve started and applied backwards. A fixed, disclosed rule is a constraint you can trade around. A rule that arrives overnight and reaches into trades you already closed is something else entirely, and it’s the mechanism behind the worst documented cases, like the $3,200 balance clawed down to $751.62. If a firm’s terms are vague enough to be reinterpreted later, or if support won’t give you a straight answer on whether a cleared payout can be reversed, treat that silence as the answer.

If you’ve ever suspected the model was working against you, you weren’t imagining it, you were reading the incentives correctly. The fix isn’t to quit, it’s to trade somewhere the incentive runs the other way. See how AI Prop’s Pass-First-Pay-Later model, on-chain payouts, and zero friction rules line up with your success rather than against it at aiprop.com.